You’ve spent your working life in the “accumulation stage” - implementing a savings discipline and a strategy -, but are now querying how and when to use these funds to support your retirement. This shift in ideology– from save to spend - is a challenge and often a cause of investor anxiety.

Life-expectancy, future health and care needs, inflation and investment performance, present challenges that are both known and unpredictable [simultaneously].

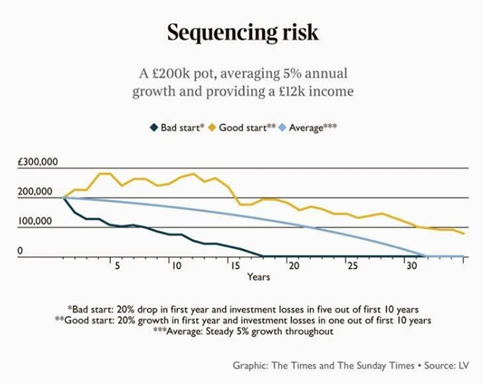

Analysis demonstrates that the best long-term outcome is available by leaning into the volatility associated with stocks and shares investment, but this opens the door to ‘sequencing risk’.

Sequencing risk relates to the negative impact withdrawals at the ‘wrong’ time (when market values are depressed) can have on the overall story. The problem is two-fold … there’s the poor value at which those assets are realised AND the opportunity cost of this withdrawal (no further capital growth potential and no further income produced).

If this event happens at the start of a retirement journey then capital is eaten away and as a result, the cashflow modelling over the entire cycle is disproportionately influenced. For simplicity, a 4% average return/yield on £100,000 may meet income requirements for life (£4,000pa)without eroding the pot, whereas if the same gross withdrawal reduces the pot to £96,000 in year-one, wealth may then diminish for life.

To mitigate this risk, there are many tactics that a retiree can invoke: -

i) Live off the income produced by the portfolio, namely dividends and interest. By using this methodology monies will never run out (capital is preserved) and will remain fully invested, but income will be restricted and fluctuate over the lifespan – difficult for budgeting and absorbing shocks.

ii) Taking a percentage of the total fund value can increase the ‘take-home’ when compared with ‘option i’ but it too will create income variants from year-to-year. An annual ‘cap and collar’ approach is statistically proven to elongate/de-risk this strategy – essentially, performance is reviewed yearly with your finance professional and withdrawals are ‘remapped’.

iii) Ring-fencing sufficient cash to provide over the shorter-term (18mo say) and then utilising the residual sums to assemble a diversified portfolio which spans the time and risk horizons. This structure can protect income requirements during downturns and thus provide the necessary time for markets to recover. The danger here is that markets trend upwards, so in most time-periods the monies that are held in cash [or similar] will create a lag in performance, which is then compounded.

iv) An approach which begins the retirement journey with less equity exposure and pivots towards the financial markets later in life – “rising equity glide path”. This diminishes the impact of sequencing risk at the start but creates drag in bull market conditions (which are statistically more likely than their Ursidae opposites)

The control and monitoring of living expenses and non-essential expenditure is an important element in any plan, and remains within the direct control of the retiree. This sits alongside the annual reviews you conduct with your independent financial adviser and the plan that is implemented (reflecting needs, fears and desires – peace of mind is crucial[even though it costs]). As with all financial conundrums the variables are wide-ranging and each individual story will be different, so control the controllables.

We strongly believe in the benefits of developing long-lasting relationships with our clients.

We aim to be approachable, easily contactable and offer a broad, inter-discipline, assessment of client needs. We are happy to meet via telephone or virtual meeting, but still prioritise face-to-face meetings where possible.

We work closely across our departments to ensure that specialist knowledge and experience is accessed; when queries arise, there will always be someone available who understands and can deal with your concerns.

We are also keen to work alongside other key stakeholders and individuals; land agents, accountants, your existing solicitor or financial adviser, and of course, your family.

As a firm we are keen to promote and involve ourselves in the community, and to support local charities and initiatives, such as Jeremiah’s Journey, St. Lukes, the Plymouth Argyle Community Trust (Project 35), Emotional Logic and the Ivybridge Brewery.

The South West is a beautiful places to live and we are proud to be based here, we’re therefore keen to help where we can.

Start the process using this form and one of our expert team members will be in touch with you shortly.